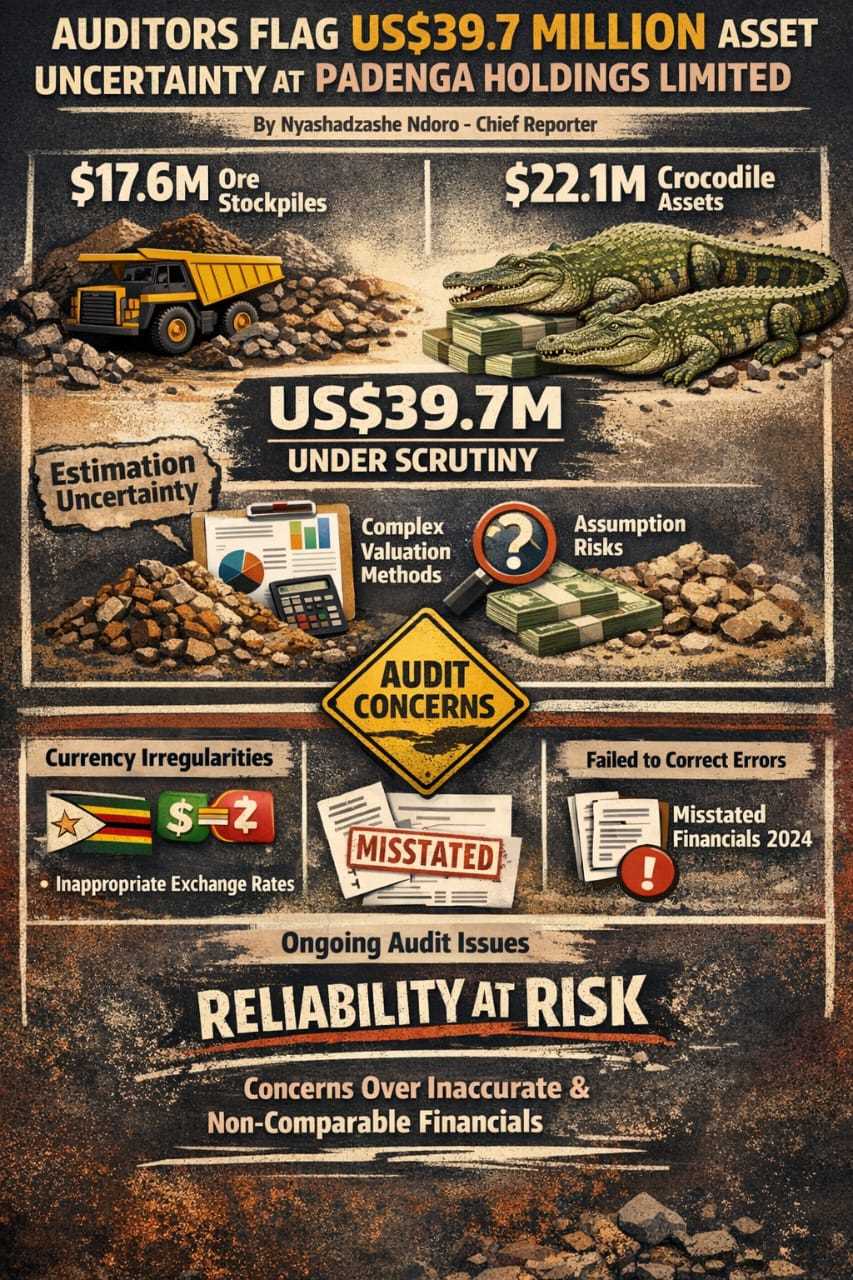

Auditors have raised concerns over the reliability of key asset valuations at Padenga Holdings Limited, flagging US$39,7 million worth of assets as exposed to significant estimation uncertainty, accounting irregularities and weak financial comparability.

In a qualified audit opinion, auditors highlighted risks surrounding ore stockpiles valued at US$17,6 million and biological assets — primarily crocodile stock — worth more than US$22,1 million, warning that complex assumptions underpinning these figures limit verification certainty.

The ore stockpiles, central to the group’s gold mining operations, were identified as a key audit matter due to reliance on estimation techniques involving volume calculations, mineral grades and density assumptions prepared by management specialists.

Auditors said the inventory measurements depend heavily on quantity surveying methods using specific gravity factors and estimated ore volumes, creating inherent valuation uncertainty.

Beyond mining assets, auditors also raised concerns over the valuation of biological assets, which include breeder and harvesting crocodiles.

“The group applies certain assumptions, judgements and uses unobservable inputs in determining fair value of biological assets,” the auditors noted.

Harvesting crocodiles are measured using a market-based valuation approach, while breeder crocodiles are assessed using replacement cost models. The valuations depend on forward-looking assumptions such as expected skin prices, productivity rates, lifespan projections and discount rates — factors that introduce significant estimation risk into the financial statements.

More serious concerns stem from historical accounting decisions linked to the company’s transition from Zimbabwean dollar reporting to US dollar functional currency in 2019.

Related Stories

Auditors found that exchange rates applied during the transition did not comply with International Accounting Standards Board requirements under IAS 21 — The Effects of Changes in Foreign Exchange Rates.

The audit report further noted that subsidiary Dallaglio Investments (Private) Limited used an incorrect date when changing its functional currency, compounding reporting inaccuracies across consolidated financial statements.

Auditors said the financial impact of these departures could not be reliably quantified due to the absence of a compliant exchange rate, but confirmed the matter was material.

The group was also criticised for failing to restate earlier financial statements in line with IAS 8 — Accounting Policies, Changes in Accounting Estimates and Errors.

As a result, balances relating to property, plant and equipment, deferred tax, depreciation and income tax expenses from the 2024 comparative period remain misstated, limiting meaningful comparison between reporting periods.

The unresolved issues formed part of the basis for the qualified audit opinion issued on the group’s latest financial statements.

Auditors noted that the accounting challenges are longstanding. The company has received modified audit opinions since 2019, following an adverse opinion issued for the 2018 financial year linked to similar currency-related non-compliance.

Despite the highlighted issues, auditors concluded that the financial statements present a fair view of the group’s position “in all material respects” except for the matters giving rise to the qualification.

Leave Comments